Financial analysis

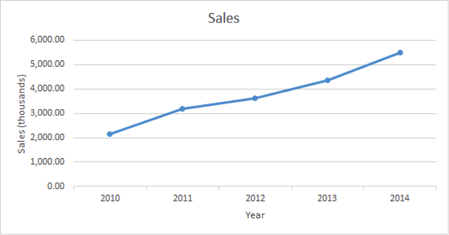

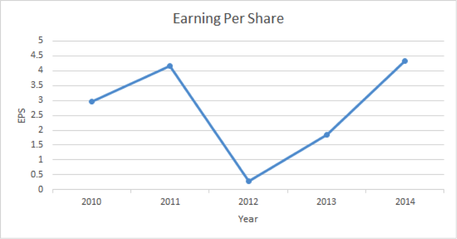

Since 2010, Netflix's revenue has seen a steady increase from year to year with an average growth rate of 26.31%. In contrast, earnings per share has seen large fluctuations over the same period due to changes in costs and marketing, consequently affecting net income. Logically, it makes sense that Netflix’s revenue is continually increasing as income is solely produced through subscription fees. The revenue generated from subscriptions increases in proportion to the increase in subscribers. However, Netflix’s profit margins are minimal due to the high costs of acquiring rights and licenses from providers to stream content. While Netflix has observed great success in the domestic North American market, the international market is trailing behind financially.

Netflix’s primary goals involve global expansion and more extensive content selection. These objectives are driven by increasing competition in the industry, and a desire to capture additional market segments. Both expansion and increased investments in content, provide no guarantee for profit, as Netflix cannot guarantee that this will motivate their customers to choose their service over their competitors.

Netflix estimates that there are over 10.5 million illegitimate consumers using their services without paying. These users have circumvented the rules by sharing accounts with friends, all who are living in different households. Netflix does allow five users per account, however, this offering is intended for families residing under one roof. At the time this research was conducted, Netflix estimated an additional 20% potential customer base based off these sharing users. If these were paying subscribers, it would add a projected 1.2 billion dollars to Netflix’s revenue per year.

Although Netflix’s income is positive, its cash flow is negative, indicating that the firm is spending more than what is shown in the company report. In 2014 Netflix made $266 million in net income on $5.5 billion in revenue but their cash flow is at - $126 million. This occurred because Netflix amortizes the cost of acquiring content throughout the life of the video license. To combat this issue, Netflix may need to consider reducing spending by slowing expansion or raising subscriptions prices for more revenue to support increased spending.

Many analysts are positive about Netflix stock and have increased their target prices, consequently giving the company a “buy” rating. However, some experts are bearish towards the stock as it is likely to become more difficult for Netflix to generate profits as more competitors are entering the market cutting into their market share. As a result, they have given a “hold” or “sell” rating for Netflix stock.

Netflix’s primary goals involve global expansion and more extensive content selection. These objectives are driven by increasing competition in the industry, and a desire to capture additional market segments. Both expansion and increased investments in content, provide no guarantee for profit, as Netflix cannot guarantee that this will motivate their customers to choose their service over their competitors.

Netflix estimates that there are over 10.5 million illegitimate consumers using their services without paying. These users have circumvented the rules by sharing accounts with friends, all who are living in different households. Netflix does allow five users per account, however, this offering is intended for families residing under one roof. At the time this research was conducted, Netflix estimated an additional 20% potential customer base based off these sharing users. If these were paying subscribers, it would add a projected 1.2 billion dollars to Netflix’s revenue per year.

Although Netflix’s income is positive, its cash flow is negative, indicating that the firm is spending more than what is shown in the company report. In 2014 Netflix made $266 million in net income on $5.5 billion in revenue but their cash flow is at - $126 million. This occurred because Netflix amortizes the cost of acquiring content throughout the life of the video license. To combat this issue, Netflix may need to consider reducing spending by slowing expansion or raising subscriptions prices for more revenue to support increased spending.

Many analysts are positive about Netflix stock and have increased their target prices, consequently giving the company a “buy” rating. However, some experts are bearish towards the stock as it is likely to become more difficult for Netflix to generate profits as more competitors are entering the market cutting into their market share. As a result, they have given a “hold” or “sell” rating for Netflix stock.

|

|

Ratios

Netflix’s ROE has increased from last year’s 10.81% to 16.67%. This ratio is important as it helps investors understand the profitability of the company. As this value has increased significantly within the year, the firm’s profitability factor has improved. Based on this ratio, Netflix is an attractive option for investors, as it provides a healthy return.

Netflix’s ROA has increased since 2012 from 0.48% to 2.43% in 2013, and now 4.22% in 2014. This shows that Netflix is becoming more efficient at converting investments into income. However, in 2011 ROA was at 13.04%, indicating this increase isn’t exactly the good news story it might appear. This 2011 to 2012 decrease can be attributed to large purchases of assets and a resulting decrease in income. Since 2011 total assets have increased from 3.069B to 7.056B in 2014, while net income increased from 226.1m to 266.8m.

The current ratio is 1.48 indicating that Netflix will be able to pay off their liabilities if they were due now. This also demonstrates that the company is in good financial health.

Although the debt to equity ratio is relatively low at 0.48, Netflix increased its long term debt by 80% from 2013 to 2014. This was the debt it used to fund global expansions and original content production. With debt to asset ratio on the lower side at 0.13 this shows that Netflix does not use much debt to fund its assets.

Netflix’s ROA has increased since 2012 from 0.48% to 2.43% in 2013, and now 4.22% in 2014. This shows that Netflix is becoming more efficient at converting investments into income. However, in 2011 ROA was at 13.04%, indicating this increase isn’t exactly the good news story it might appear. This 2011 to 2012 decrease can be attributed to large purchases of assets and a resulting decrease in income. Since 2011 total assets have increased from 3.069B to 7.056B in 2014, while net income increased from 226.1m to 266.8m.

The current ratio is 1.48 indicating that Netflix will be able to pay off their liabilities if they were due now. This also demonstrates that the company is in good financial health.

Although the debt to equity ratio is relatively low at 0.48, Netflix increased its long term debt by 80% from 2013 to 2014. This was the debt it used to fund global expansions and original content production. With debt to asset ratio on the lower side at 0.13 this shows that Netflix does not use much debt to fund its assets.